Corporate tax rates play a crucial role in shaping the economic landscape of a country, influencing business investments, job creation, and overall economic growth. The debate surrounding these rates has intensified since the passing of the 2017 Tax Cuts and Jobs Act, a landmark reform that significantly reduced corporate tax rates from 35% to 21%. Supporters of corporate tax cuts argue that these reductions encourage more investments and are essential for fostering both domestic and foreign business growth. However, critics caution that such cuts may disproportionately affect federal tax revenue and exacerbate economic disparities. Analyzing the economic impacts of tax policy is essential as lawmakers continue to grapple with the future direction of corporate taxation amid changing global dynamics and economic challenges.

The topic of corporate taxation, including its rates and the associated implications for businesses, is increasingly relevant in today’s political and economic discourse. Often referred to as corporate income taxes, these rates directly impact how much companies contribute to federal and state revenues. Discussions around tax cuts for corporations became prominent following the transformative 2017 tax reform, which lowered the statutory rate significantly. As policymakers and economists evaluate the broader consequences of such tax policies, it is vital to consider not only immediate fiscal impacts but also long-term effects on innovation and workforce growth. By exploring variations in tax incentives and their influence on corporate behavior, stakeholders can better navigate this complex landscape.

Understanding Corporate Tax Rates: An Overview

Corporate tax rates play a pivotal role in shaping the economic landscape of any country, influencing business decisions and investments. In the United States, the corporate tax rate was significantly altered by the Tax Cuts and Jobs Act (TCJA) of 2017, which slashed the statutory rate from 35% to 21%. This drastic reduction aimed to spur economic growth by encouraging businesses to reinvest profits back into the economy. Consequently, companies could allocate more resources towards expansion, innovation, and hiring, thus impacting overall economic growth positively.

The implications of corporate tax rates extend beyond mere percentages on profit margins. They interact with various facets of economic policy, such as investment incentives and labor market dynamics. For instance, lower corporate tax rates can boost capital investments by allowing firms to retain a larger share of their earnings. This phenomenon was observed post-TCJA, where certain provisions incentivized immediate write-offs of capital expenditures, leading to an 11% increase in capital investments. Understanding these dynamics is crucial for evaluating the effectiveness of tax policies in promoting sustainable economic growth.

The Impact of the 2017 Tax Cuts and Jobs Act on Corporate Strategy

The 2017 Tax Cuts and Jobs Act (TCJA) was a significant event in U.S. economic policy, prompting corporations to reevaluate their investment strategies amidst the backdrop of reduced corporate tax rates. Following the enactment of the TCJA, corporations were presented with both opportunities and challenges. On one hand, the lowered tax burden allowed companies to hold onto more profits, theoretically enabling increased investments in technology, workforce training, and expansion projects. On the other hand, the immediate loss in tax revenue raised questions about long-term fiscal sustainability and the need for careful strategic planning.

Moreover, corporate leaders found themselves at a crossroads concerning their operational goals versus tax minimization strategies. The TCJA introduced various business investment tax incentives, like immediate expensing of capital investments, which drove many firms to channel their resources toward innovation and growth. However, with the ongoing discourse on possibly raising corporate tax rates to replenish federal revenue, organizations must remain agile to adapt to potential shifts in tax policy that could alter incentive structures. This underscores the need for sound strategic planning that balances growth objectives with prudent tax considerations.

Economic Impacts of Tax Policy: A Closer Look

Understanding the economic impacts of tax policy, particularly corporate tax rates, requires careful examination of the data. Post-TCJA, critics and proponents alike have debated the tangible benefits of corporate tax cuts. Initial analyses showed modest wage increases and a boost in capital investments, suggesting that the 2017 reforms had some positive effects on the economy. However, the anticipated large-scale benefits, such as significant wage increases per employee, were far less than proponents had predicted, suggesting a more nuanced interpretation of the law’s effects is necessary.

Further empirical studies highlighted the complexities in how corporate tax cuts influence broader economic conditions. For instance, while some businesses did invest more aggressively due to lower tax burdens, others did not significantly change their investment strategies. This variability showcases the importance of industry-specific factors and the broader economic environment in determining the effectiveness of tax cuts as an economic stimulus. Policymakers should consider these findings in future tax reforms, ensuring that changes in corporate tax rates effectively align with desired economic outcomes.

Business Investment Tax Incentives: Driving Growth

Tax incentives aimed at business investments, particularly those introduced in the TCJA, are vital for stimulating economic growth. These incentives allow corporations to deduct the full cost of certain investments from their taxable income in the year they are made, thereby promoting immediate spending on capital projects. The rationale behind such policies is straightforward: when firms are encouraged to invest in infrastructure, technology, and R&D, they can potentially create jobs and enhance productivity in the long run.

However, the impact of these incentives is still up for debate. Critics argue that while some businesses benefit from these advantages, others either lack the capital to invest or may choose not to take full advantage of the incentives. Therefore, it becomes imperative for lawmakers to craft targeted incentives that not only encourage investment but also consider the varying capacities of firms across different industries. Future tax reforms should aim to create a balanced and equitable tax landscape that effectively promotes business investments and stimulates economic growth.

The Debate on Raising Corporate Tax Rates

The discourse surrounding the potential increase in corporate tax rates is highly polarized, with significant implications for the economy. As we approach 2025 when several TCJA provisions are poised to expire, leaders from both sides of the political spectrum are weighing in on whether raising the corporate tax rate is advisable. Proponents of higher rates argue that it could generate necessary revenue for social programs and infrastructure, directly contributing to public welfare and economic stability.

Conversely, opponents contend that increasing corporate tax rates could stifle business growth and deter investment. They argue that higher taxes might lead to reduced capital expenditures and job creation, ultimately hindering economic momentum. This ongoing debate highlights the need for balanced tax policies that consider not only the fiscal health of the government but also the competitive landscape in which businesses operate. Future discussions should focus on crafting tax strategies that rouse economic growth while ensuring sustainable government revenue.

Lessons Learned from the Tax Cuts and Jobs Act Analysis

The analysis of the TCJA reveals critical lessons regarding the relationship between corporate taxation and economic behavior. The collaboration between Harvard, Princeton, and the University of Chicago researchers, led by Gabriel Chodorow-Reich, underscores the necessity of empirical evidence in assessing tax policy effectiveness. While the TCJA was heralded for its corporate tax cuts, the reality illustrated that these cuts did not single-handedly ‘pay for themselves’ through increased investment as many advocates proclaimed.

This insight suggests that policymakers need to temper their expectations regarding tax cuts. The findings highlight the importance of incorporating a mix of strategies, including investment incentives and potential statutory rate adjustments, in future tax legislation. The lesson is clear: a nuanced approach that combines various elements of tax policy could better serve the economy than a one-size-fits-all reduction in corporate tax rates.

Evaluating Wage Impacts Post-TCJA

The impact of the TCJA on wages provides a fascinating glimpse into the complexities of tax policy outcomes. While the Council of Economic Advisers suggested substantial wage increases were imminent, subsequent studies revealed a much lower average wage boost for employees following the enactment of the TCJA. Such findings have engendered a critical re-evaluation of the assumptions surrounding how tax cuts translate into tangible benefits for everyday workers.

This discrepancy between expectations and actual outcomes reflects the multifaceted nature of wage dynamics within the corporate sector. For instance, while some industries may benefit more from tax cuts due to higher profit margins and reinvestment capabilities, others may not experience significant wage increases at all. This highlights the necessity for more targeted fiscal policies that not only consider large corporate entities but also aim to uplift wages for the workforce through more inclusive economic policies.

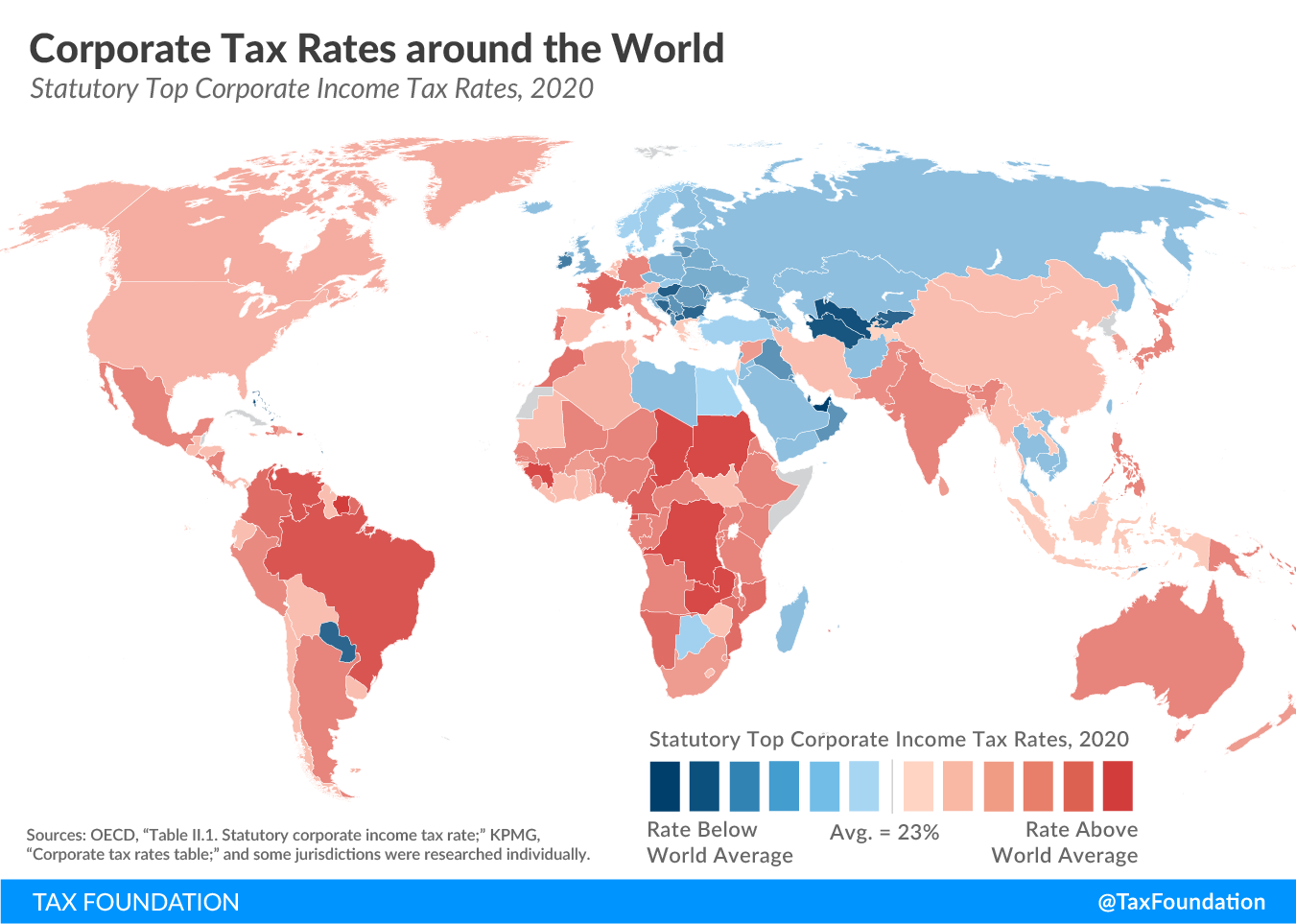

The Future of Corporate Taxation in a Globalized Economy

As international competition continues to evolve, the future of corporate taxation will require innovative thinking and strategic adjustments. The global landscape has changed dramatically since the TCJA, compelling many countries to reassess their corporate tax structures to remain competitive. As the U.S. attempts to address its corporate tax rates, policymakers must consider how changes will influence not only domestic firms but also multinational corporations operating across various jurisdictions.

This process involves understanding the delicate balance between maintaining competitive tax rates that stimulate domestic investment while ensuring adequate revenue generation for essential public services. Future reforms may necessitate establishing a more comprehensive tax framework that considers both domestic and international factors, promoting equitable competition among nations while also fostering a climate for innovation and growth on American soil.

Insights from Corporate Tax Revenue Trends

Analyzing trends in corporate tax revenue reveals much about the effectiveness of tax policies and the economic landscape. After the implementation of the TCJA, there was a dramatic drop in corporate tax revenue, which raised alarms about fiscal sustainability. However, subsequent years showed a surprising rebound in corporate tax receipts as profits surged. This trend underlines the complex relationship between corporate tax rates and actual revenue generation, challenging the notion that lower rates will always lead to diminished revenue.

The fluctuating nature of revenue collection stresses the importance of ongoing evaluations and adjustments to corporate tax policy. As companies adapt to shifting economic conditions, understanding the underlying factors contributing to profitability and tax liabilities can guide future legislative decisions. It highlights the necessity for data-driven insights and the responsiveness of tax policy to maximize revenue while fostering a healthy business environment.

Frequently Asked Questions

What are the corporate tax rates following the Tax Cuts and Jobs Act of 2017?

The Tax Cuts and Jobs Act of 2017 permanently reduced the corporate tax rate from 35% to 21%. This significant change was part of an effort to make the U.S. tax code more competitive globally and to encourage business investment.

How have corporate tax cuts impacted business investment since the 2017 tax reform?

Research suggests that corporate tax cuts under the 2017 tax reform led to approximately an 11% increase in capital investments. This was primarily driven by expiring provisions that allowed firms to fully write off new investments, demonstrating a positive correlation between corporate tax rates and business investment.

What were the economic impacts of the corporate tax cuts included in the 2017 Tax Cuts and Jobs Act?

The economic impacts of the corporate tax cuts included modest increases in wages and business investments; however, corporate tax revenue initially declined by 40%. Despite this, corporate tax revenue rebounded significantly starting in 2020, fueled by unexpectedly high business profits.

How do business investment tax incentives work under the current corporate tax rates?

Under the corporate tax rates established by the 2017 Tax Cuts and Jobs Act, business investment tax incentives such as immediate capital expensing allow companies to deduct the full cost of new equipment and investments in the year they are incurred, thus promoting higher rates of capital investment and stimulating economic growth.

What are the potential changes to corporate tax rates expected in 2025?

With key provisions of the Tax Cuts and Jobs Act set to expire in 2025, there is an ongoing debate in Congress regarding whether to raise the corporate tax rates back to previous levels or maintain them at the current rate. Both sides of the political spectrum are considering different approaches to corporate taxation to address budgetary needs.

What lessons can policymakers learn from the corporate tax cuts of the 2017 tax reform?

Policymakers can learn that while corporate tax cuts may spur business investments, as shown in the 2017 tax reform, the relationship between tax rates and corporate behavior is complex. Evidence indicates that targeted incentives rather than broad rate cuts may lead to more effective economic outcomes.

Will raising corporate tax rates have a negative effect on business investment?

While there is concern that raising corporate tax rates could discourage business investment, evidence from the analysis of the 2017 tax reform indicates that targeted tax incentives can amplifying investment levels even amid higher rates. Thus, a balanced approach may be necessary.

How do corporate tax cuts affect wage growth?

The impact of corporate tax cuts on wage growth is debated. The Council of Economic Advisers previously projected significant wage increases due to tax reforms, but recent analyses suggest more modest increases, estimated at around $750 per year per employee, highlighting the need for careful consideration of economic policies.

What factors contributed to the surge in corporate profits after the Tax Cuts and Jobs Act was enacted?

Several factors contributed to the surge in corporate profits post-TCJA, including improved profitability tied to business strategies during the pandemic and changes in corporate behavior. Additionally, external factors like tax policy shifts in places like Ireland made the U.S. more attractive for profit reporting.

What to expect from the upcoming tax policy debates regarding corporate tax rates?

In the lead-up to 2025, expect heated debates on corporate tax rates as lawmakers consider the expiration of various provisions from the TCJA. Both parties are likely to propose differing strategies for taxation and potential reforms aimed at business investment and revenue generation.

| Key Points |

|---|

| Corporate Tax Rates are under debate as key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) near expiration, sparking evaluations of their effectiveness. |

| Gabriel Chodorow-Reich’s study explores the impact of TCJA corporate tax cuts, revealing modest increases in wages and business investments, and urging a review of partisan narratives. |

| The TCJA permanently reduced the corporate tax rate from 35% to 21%, projected to lower federal tax revenue by $100-150 billion annually over a decade. |

| There are calls for reform, with possibilities of raising statutory rates while restoring expensing provisions for new capital investments. |

| Chodorow-Reich argues that while corporate tax cuts theoretically promote investment, evidence suggests targeted expensing measures yield better results. |

| The federal corporate tax revenue initially plummeted by 40% but increased significantly as business profits soared post-TCJA, highlighting unexpected economic dynamics. |

Summary

Corporate Tax Rates are at the forefront of political debate as lawmakers assess the impact and efficacy of the Tax Cuts and Jobs Act of 2017. As key provisions approach expiration, experts are examining the law’s benefits and repercussions, indicating the need for strategic reforms to optimize tax revenue while fostering investment. The ongoing discussions surrounding Corporate Tax Rates are shaping the fiscal landscape leading into 2025, making this a crucial time for policymakers to navigate complex economic realities.